International Trade: Mirror & Engine of Geopolitics & Tech

Trade patterns, tech breakthroughs, and geopolitical shifts rarely move in isolation. There’s never been a better time to watch international trade; it is both mirror and engine for changes in tech and geopolitics.

Words by

Sean Yu

12 months or so ago I was on the phone with my dad, arguing that Trump is good for gold and copper but pretty much bad for everything else. It was a weird fight before Thanksgiving that led me to skip going home. But I had noticed: gold prices weren’t really tracking interest rates the way they used to, and copper demand wasn’t coming from the usual suspects like infrastructure and real estate anymore. I dug into gold’s trade flows, and it was clear central banks were anxious—buying physical gold, moving it across borders, stockpiling reserves. Then copper: getting bid up by data-center builds and grid equipment for AI as nations race toward AGI. Something had shifted. I could smell it. That brings us to Geopolitics, Technology, and International Trade. Let me walk you through what I mean. Once you see this pattern, it changes how you understand almost everything happening in the world right now

Techno-Geopolitics-Trade Spiral

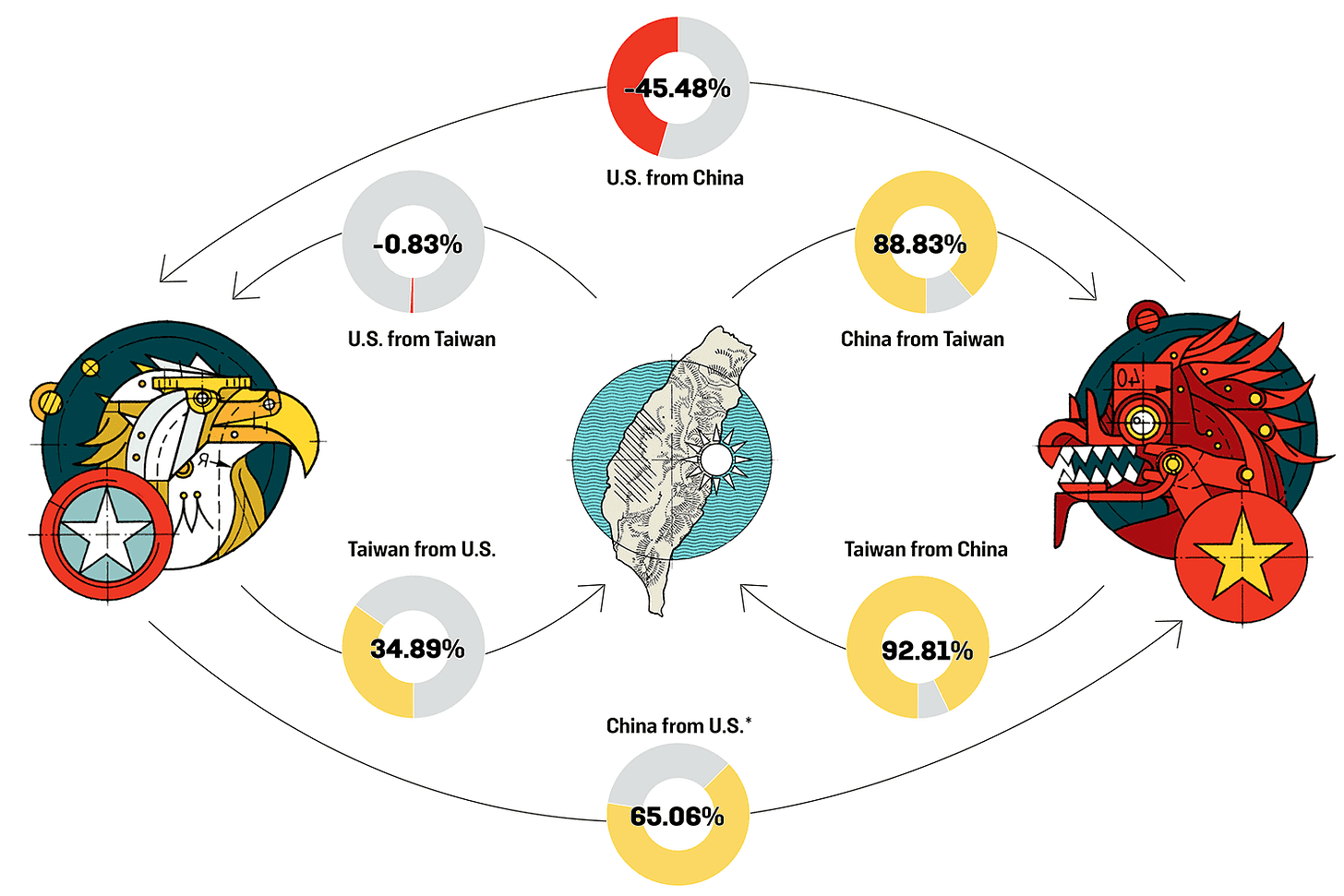

30 years ago, a small island in East Asia decided to go all in on chipmaking. Today, one company there—TSMC in Taiwan—produces 90% of the world’s most advanced chips.

Every day these engineered parts leave Taiwan on cargo planes and container ships, heading to assembly plants in China, design firms in California, equipment makers in Germany, defense contractors in Virginia.

This is one of the densest trade flows in the modern economy. In 2023, Taiwan exported roughly $166.6 billion of integrated circuits; over $90 billion of that went to China. The flow is a circulatory system for global tech.

Now geopolitics exerts its force. Taiwan sits on the First Island Chain—the arc from Japan through Taiwan and the Philippines that bounds China’s access to the wider Pacific. Around 80% of China’s oil imports pass through the Strait of Malacca and the South China Sea. Location matters. Taiwan’s chip dominance makes it matter even more to the United States. People call this the “silicon shield”: TSMC’s prowess gives Taiwan leverage in a tense neighborhood.

So why did TSMC concentrate in such a contested location? Because when TSMC was taking off, U.S. policymakers broadly believed economic interdependence would moderate conflict with China, and China’s tech base lagged far behind. Supply-chain efficiency ruled. Morris Chang executed brilliantly—pioneering the pure-play foundry model, pouring into R&D, and building an ecosystem that’s brutally hard to copy. By the time people woke up to the strategic implications, trade patterns were locked in, chips were flowing, and dependencies were built.

For years, analysts wondered whether a military clash over Taiwan would happen. The mutual tech-trade dependence created strong incentives against escalation: China needed access to leading-edge chips while it built its own industry; any conflict would cut that off overnight as the U.S. and allies tightened controls. Dependence, paradoxically, helped restrain confrontation—until it didn’t.

Then the spiral kicked in.

Beijing looked at the vulnerability and said, we need semiconductor self-sufficiency. Under Made in China 2025, China set a target of 70% domestic content in key technologies by 2025, including semiconductors. That geopolitical response triggered huge tech programs: tens of billions for research, fabs, talent. Washington answered with the most far-reaching export controls in decades in October 2022 (FDPR expansions and advanced-computing rules), and pressed TSMC to add U.S. capacity. It also leveraged its allies such as Netherland to bar EUV & DUV to China, in parallel, U.S. Entity List and FDPR measures restrict specific Chinese firms and some ‘U.S. persons’ support. These are trade compliance tools deployed for geopolitical aims that reshape technology’s geography.

Most recently, late October 2025, Trump and Xi met in South Korea and agreed to a limited one-year trade truce that trims some tariffs and pauses parts of the escalation cycle. It softens edges, but it doesn’t resolve the structural clash.

The same loop plays elsewhere.

The energy race

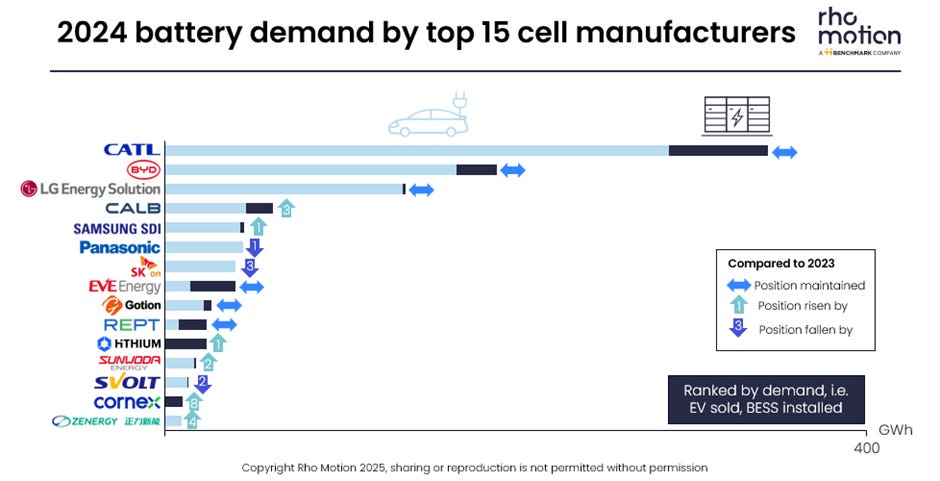

Battery pack prices have fallen roughly 90% over the past decade-plus and dropped another ~20% in 2024. China now produces over three-quarters of the world’s batteries and holds cost advantages from scale and integrated supply chains. In 2024, China exported about $177 billion of clean-tech hardware (solar panels, EVs, batteries, wind), and the exports keep climbing. This is trade dominance.

Dominance becomes leverage. When China hints at export restrictions on inputs like graphite, gallium, or germanium, is that technology policy, trade policy, or geopolitical strategy? The categories blur because the effects are the same. The U.S. IRA responds with strict FEOC sourcing rules: batteries with components or critical minerals from certain entities don’t qualify for credits. The EU has pushed to meet ~90% of battery demand from European production by 2030—an ambition that remains at risk but guides policy. These political interventions immediately accelerate tech build-out, from Korean and Japanese firms adding LFP lines to U.S. and EU plants. Note: Nissan announced an LFP battery plant in Japan in January 2025, then canceled it in May 2025; plans are shifting fast.

Each trade restriction speeds up rival investment. Each technology breakthrough shifts bargaining power. The spiral turns, and trade is the medium.

Trade compliance as a mirror to geopolitics & tech diffusion

Tech billionaires funded politicians love trade compliance, but they don’t talk about it loudly

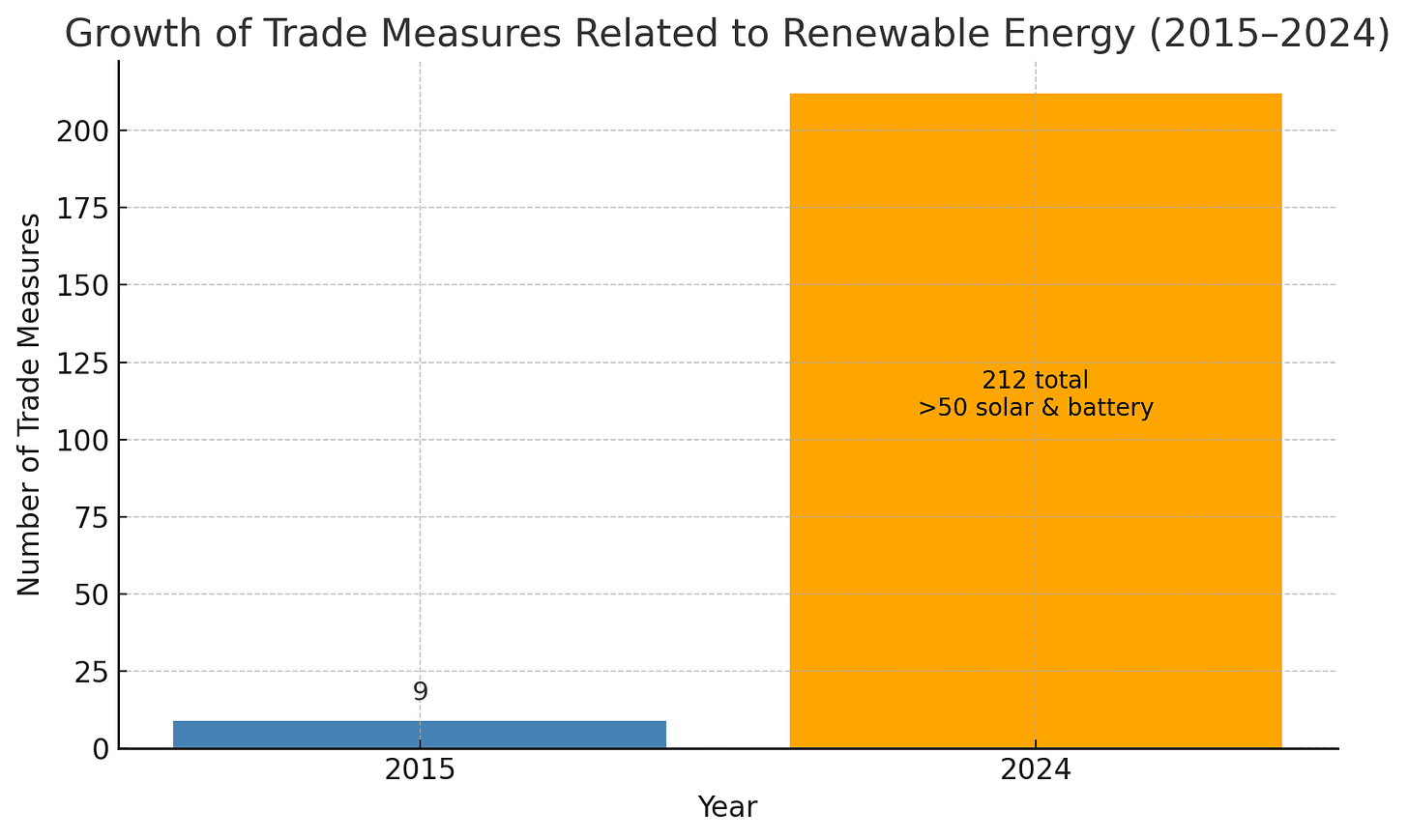

In 2015, there were only 9 formal trade measures related to renewable energy and enabling technologies. By 2024, that number jumped to 212—including over 50 policies each targeting solar panels and battery components. Why did trade policies explode like that? Because renewable energy represents energy sovereignty from fossil fuel and hence dollars, it is also a training ground for manufacturing which could be turned into military power base when necessary without giving the public “war fears”. Hard to find reasons not to love it as a rule maker.

When the U.S. tightens chip controls, you’re seeing a misalignment declared in the language of compliance. When Japan, Korea, and the U.S. align frameworks, you’re watching alliance structure show up in proclamations. When China restricts rare-earth-adjacent materials, you’re watching technology leverage expressed as an export rule.

Trade compliance is like a rearview mirror that allows you to peek into what critical shifts took place in geopolitics & tech world without reading all about it.

Trade as an engine

A country outcompetes with superior technology, and technology spreads through trade. Marry great tech to great trade routes and you increase the odds of outsized influence.

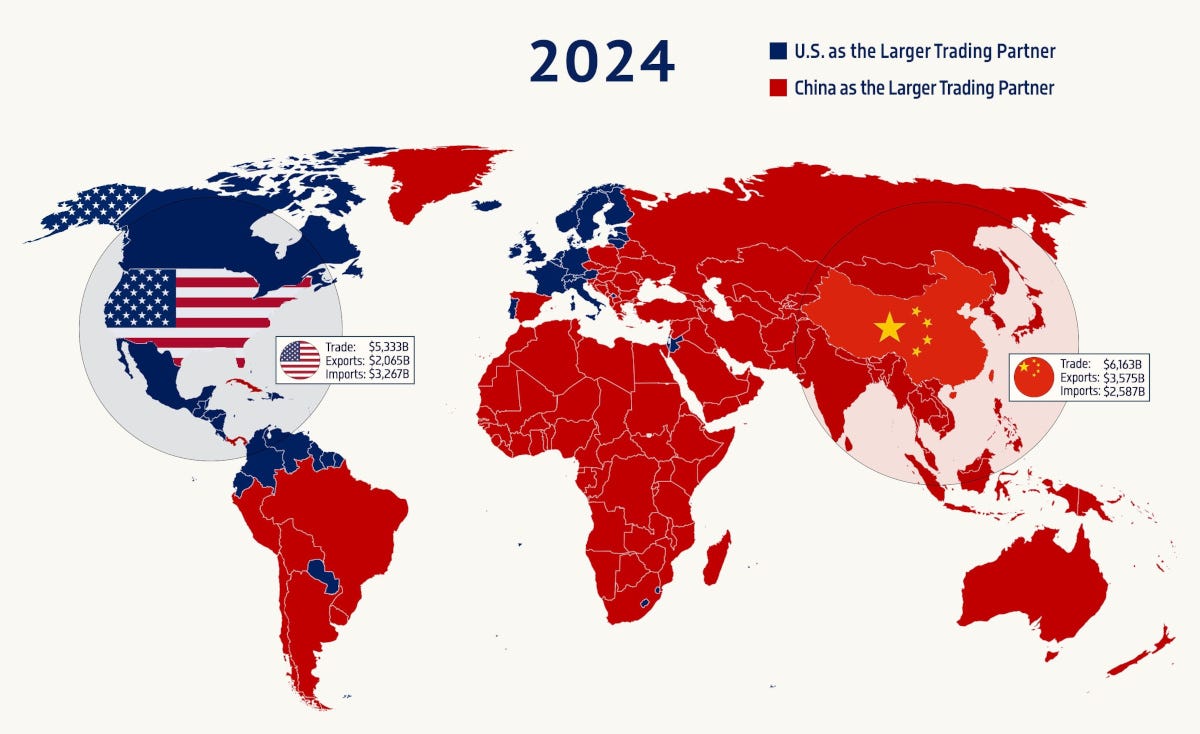

China’s geological location makes it vulnerable to energy supply disruptions, unless it has a good relationship with its neighbour Russia (who took lands from China a little over a century ago), this makes it determined to invest heavily in energy transitions.

Europe is the test case. Battery production still costs more in the EU than in China—up to ~45% more depending on segment—because of energy, labor, and scale. That cost gap, plus China’s Belt-and-Road market access, opened Europe to Chinese clean-tech exports and created the political pressure for subsidies and domestic champions. Europe started building a battery strategy in 2018—earlier than major U.S. moves like the 2022 CHIPS/IRA packages—but scale remains the hurdle.

Why does Europe care about batteries so much? Because the same industrial base that builds batteries and power electronics underpins surge capacity for defense—factories, skilled labor, machine tools, and supply chains. Europe’s struggle to hit its 1-million-shell pledge by March 2024, and the subsequent push to ramp 155 mm output toward ~2 million rounds per year in 2025, shows how industrial slack limits defense readiness. This isn’t “no chance of defending itself,” but it is a constraint: without competitive energy-and-manufacturing capacity, Europe’s ability to sustain production in a long crisis weakens. NATO leaders have said the quiet part out loud—Europe must spend more and scale production faster.

Trade competition is where tech strength and geopolitical positioning get exercised. It often starts with free trade and ends with protection. Watch the trades and you can often see tomorrow’s alliances and tech clusters forming.

Old world order

During the unipolar moment, trade, tech, and geopolitics operated separately because the U.S. had no peer competitors, as a result, trade compliance specialists and strategists were put behind the spotlight for decades. Doing the same today however, guarantees constant surprises.

We’re living through the shake. Will the old order collapse? History says orders end. Watch the trade flows and the rule changes and you’ll see the pacing.

So if you care about geopolitics & tech as much as I do, I suggest you read about international trade, it’s the clearest lens we have right now :).